In an interview with CNBC-TV18, he said better rural cash flows driven by a healthy monsoon, strong kharif output, robust reservoir levels, and potential ramp-up in infrastructure activity in line with the government aim to meet its capital outlay target, are likely to lead to a demand rebound.

This is the verbatim transcript of the interview.

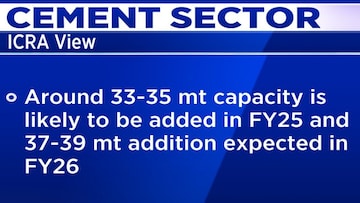

Q: The first half (H1) of FY25 was very weak as far as cement was concerned. In H2 do you expect a significantly better pickup?

A: We are expecting a healthy pickup in the second half of the current fiscal. In ICRA’s view, the likely improvement in farm cash flows backed by a healthy monsoon upbeat kharif output and healthy reservoir level is expected to boost rural consumption in the second half of FY25. So, that will drive the cement demand for the rural housing segment.

Also, if the government has to meet ₹11.1 lakh crore capital outlet target, then a significant ramp-up is also required in the infrastructure activity in the second half, which will drive growth. So, we are pretty upbeat that things will sequentially improve, while Q1 and Q2 were weak because of the slower-than-expected ramp-up in the construction activity. But we are building our hope in Q3 and Q4 on both infrastructure and ruler segments to trade the growth.

Q: So H1 volume growth was 2%. What is your volume estimate for H2?

A: Around 7-8%.

Q: Therefore, on an aggregate basis, for the full year, we should be at 4-5%. But in July, when you came out with your forecast of 7-8%, what was priced in because we know that typically elections do slow down the construction, I mean, it has an impact. Was it just the monsoon which caused a sudden shift in your assessment of growth?

A: No. What we were expecting is the ramp-up post-election because the model code of conduct is in place and there are certain challenges in the overall activity and it slows down. So, Q1 was expected to remain weak only, but in Q2 we were expecting a very healthy ramp-up in the infrastructure activity. So that has not materialised how it should have been.

Also Read: India’s GDP growth likely to slip at 6.5%, maintains 7% estimate for FY25: ICRA

And once all the elections are largely done, we are expecting a very healthy ramp-up in all the markets, especially in the western and northern markets, and things should improve sequentially. Looking region-wise, in ICRA’s view, the southern market remains under pressure, but other markets should do relatively better.

Q: One thing that we have discussed is the kind of weakness as far as demand is concerned that has also led to weakness as far as pricing is concerned. Now, given the fact that there has been significant consolidation as far as the entire industry is concerned, do you expect some sequential improvement in pricing? And what is the kind of pricing trend that you are pencilling in as far as H2, as well as FY26, is concerned?

A: A lot of pressure on the margin is largely driven by pressure on the pricing. What has come as a saviour is the overall input costs came down, so the overall impact is not as severe as it could have been. But sequentially, in the last few months, we have seen pricing going up in all the major markets, be it in the western region, northern region and eastern region. The southern region remains a lacklustre, but we are seeing around 4-7% growth at a blended level overall and we are seeing this in the last few months, especially in September and October. So that will sequentially improve.

Also Read: Experts analyse capex and infrastructure growth in key states

Is it still able to match last year’s number? The answer is no. It will remain year-on-year (YoY) lower than last year’s number. But sequentially, things are improving, and that is what industry participants are also saying, that Q3 will be better in terms of pricing, but if you look at the overall geography mix, in the southern market, we are not seeing that kind of price increase. So definitely, the performance will vary across the region in India.

Q: So ₹330 per bag was the approximate pricing in H1. Give us the number for Q3-Q4 across the various geographies and have we started seeing price hikes already?

A: We are already seeing the price hikes and it ranges in the range of ₹7-14-15 and that has already happened. In certain pockets, certain companies have taken a slightly larger price hike. But we are talking about a blended level here, the price hike varies across regions. So, the price hike is much better off in the western region, northern region, also in eastern region, but when we talk about the price hike in the southern region, they are largely flattish.