What makes it work: Securitizing subprime auto loans and selling the Asset-Backed Securities to yield-hungry investors.

By Wolf Richter for WOLF STREET.

Subprime auto loans are making breathless headlines again. Subprime-rated borrowers tend to get in trouble with their debts, which is precisely why they’re rated subprime in the first place.

Only about 14% of total outstanding auto-loan balances are subprime – and most of them have been securitized into Asset Backed Securities (ABS) and sold to investors who’d bought them to get the higher yields. Typically, subprime-rated borrowers purchase older, such as 10-year-old or older, used vehicles with those loans because that’s the only thing they qualify for.

Subprime auto lending is not a factor in new vehicles. There is little subprime lending in new vehicles. New vehicles are largely reserved for prime-rated customers and for cash-buyers. New vehicle unit sales jumped 20% year-over-year to 4.08 million vehicles in the quarter through September, with the Average Transaction Price (ATP) rising to $47,420. These vehicles are not the hunting grounds of subprime-rated car-buyers.

Interest rates to finance new vehicles have risen, and buyers wince and gnash their teeth. But the captive auto lenders, such as Ford Credit, are buying down interest rates, and automakers are subsidizing leases, and prices are up, inventories are back, and new-vehicle unit sales are up 20% year-over-year.

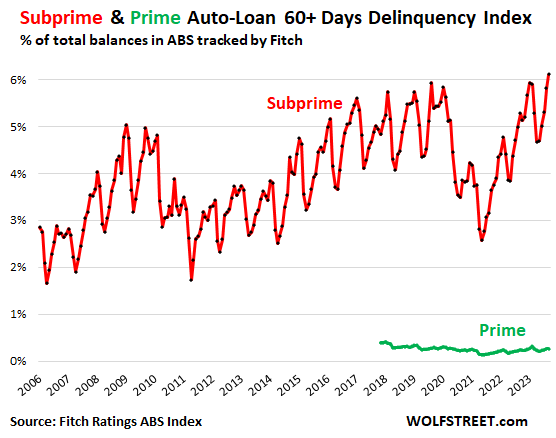

Prime-rated auto loan delinquency rates are minuscule. Prime-rated auto loans account for 86% of auto-loan balances outstanding. And they’re in pristine condition. Fitch, which rates auto loan Asset Backed Securities (ABS), reported that the 60+ days delinquency rate of prime auto loans in September was 0.27%, below where it had been in the years before the pandemic (green line in the chart below).

Where the shoe pinches is in subprime. It always does. A substantial portion of subprime auto loans is always in trouble. That’s why they’re subprime. It’s a high-risk, high-profit but relatively small corner of the used-vehicle market, and it regularly makes for breathless headlines.

The 60+ days delinquency rate of the subprime-backed ABS that Fitch tracks rose to 6.1% in September, eking past the prior record of 6.0% in October 1996 and of 5.9% in August 2019, the Good Times.

This chart shows the 60-plus days delinquency rates based on the ABS tracked by Fitch Ratings of subprime-rated borrowers (red) going back to 2006, and prime-rated borrowers going back to September 2017 (green). Remember: only 14% of all outstanding auto-loan balances are subprime, 86% are prime:

Government largess during the pandemic bailed out subprime too. People got all kinds of cash from the government, and they got mortgage forbearance and student loan forbearance and they were protected by eviction bans, and many of them used this extra cash to get caught up on their auto loans, and the subprime delinquency rate dropped to a multiyear low of 2.6% in May 2021 (just after the stimmies had gone out).

So subprime lenders got very aggressive, and some of them then blew up in 2023. This drop in the delinquency rate, backed by the general mayhem of investors chasing yield in a 0% interest-rate environment, caused specialized subprime dealers and lenders to get very aggressive, with huge loan-to-value ratios, and with loosey-goosey underwriting standards. But the fun didn’t last very long, and some specialized national chains have now blown up.

Subprime lending is a risky business – and there can be slimy aspects to it – but companies do it because it can be very profitable, with very high interest rates and huge profit margins on the vehicles, and investors pile into it because of the juicy yields.

But when the subprime dealer-lenders get too greedy, and too loosey-goosey with their lending standards, they blow up, including the two PE-firm-owned heroes that we’ve covered here:

- US Auto Sales, a 39-store specialized subprime dealer chain owned by a private equity firm shut down in April and filed for Chapter 7 bankruptcy liquidation in August.

- American Car Center, a 40-store subprime dealer chain also owned by a PE firm, shut down in late February, and in March filed for Chapter 7 liquidation.

What makes it work: Subprime auto-loan-backed ABS. Specialized subprime lenders or dealer-lenders work the same way: They make high-risk high-interest-rate loans to subprime-rated borrowers to fund the purchase of older overpriced used vehicles with huge profit margins, knowing that a substantial portion will default.

Periodically, they then securitize their pools of subprime auto loans into ABS with different tranches, from the equity and deep-junk tranches to tranches with investment-grade ratings. An equity tranche is generally retained by the dealer. The equity tranche and the lowest-rated tranches take the first losses, but they have also the highest yields. As the losses get bigger, the higher-rated tranches start to take losses.

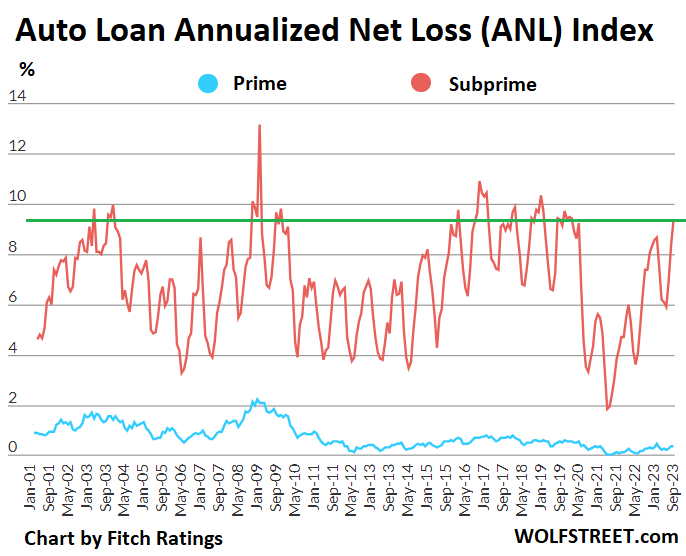

Net losses of subprime-backed ABS normalize, after free-money bailout. Fitch also tracks net losses for the auto-loan ABS that it rates.

Its prime-rated Annualized Net Loss (ANL) Index, at 0.36%, was well below the range in the years before the pandemic (in September 2019, it was 0.53%).

Its subprime-rated Annualized Loss Index rose to 9.23%, which was a tad below the same months in the years before the pandemic (in September 2019, it was 9.27%; in September 2018, it was 9.44%).

In other words, prime-rated auto-loan credit losses remain below the pre-pandemic years and are in pristine condition.

And subprime credit losses have now normalized within the seasonality of this business, compared to the same months in the years before the pandemic. But some of the PE-owned specialized subprime dealer-lenders – as is so often the case when the free money ends – blew up (chart by Fitch).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()